For businesses

For accounting & bookkeeping firms

Start a free trial

Log in

Product

Enhance your practice with Dext

Capture bookkeeping data

Capture data directly to save time and eliminate manual entry.

Automate processing

Set supplier rules or auto-categorise, and publish to your accounting software.

Improve workflows

Manage client workflows, source missing documents without the chasing.

Ensure client data health

Identify data gaps and assess data health for all clients.

Practice productivity

Access practice and client-level insight, and team efficiency measures.

Integrate accounting software

Integrate Dext with leading accounting software packages such as Xero, QBO and more.

Connect to e-commerce

Capture transactions from e-commerce shops and online marketplaces.

Simplify payments

New

All your payments securely in one place. Receive money from customers, manage expenses, and pay suppliers and employees.

Securely store documents

New

Store all essential business documents and organise them intelligently with AI.

Benefits

The value of bookkeeping automation

Why bookkeeping automation?

Real-time, complete data unlocks value. Bookkeeping automation makes this possible.

What's the return on Dext?

Dext saves time, increases productivity and improves data. But there’s more. Learn how to maximise your return on Dext.

Dext in your firm

Dext improves your client experience, makes teams more productive and streamlines workflows.

Pricing

Resources

Access support, learn and grow

The Dext Blog

Access insight, resources and knowledge to keep one step ahead.

Join Orange Select

Connect, learn, share and grow with Dext's community of accountants and bookkeepers.

Events and webinars

Discover our upcoming workshops, webinars, and training events.

Dext help centre

Get help using Dext products. Help articles, getting started guides & FAQs.

Contact us

Get in touch with Dext. Email, phone, mail and support.

New features and product updates

Learn about our latest product news, updates and enhancements to get the most out of our products and features.

Dext Hub

for your accounting news

Insight and opinion to help you grow

All

Accounting

Articles

Business

Case Studies

Resources

The Global Partner Update – Q2 2025

Published on: 29.04.2025

The next phase of the Dext evolution is here

Published on: 05.03.2025

Dext in 2025: A round-up from the Global Partner Update

Published on: 27.01.2025

2024 at Dext: Innovation and features that made your life easier

Published on: 16.12.2024

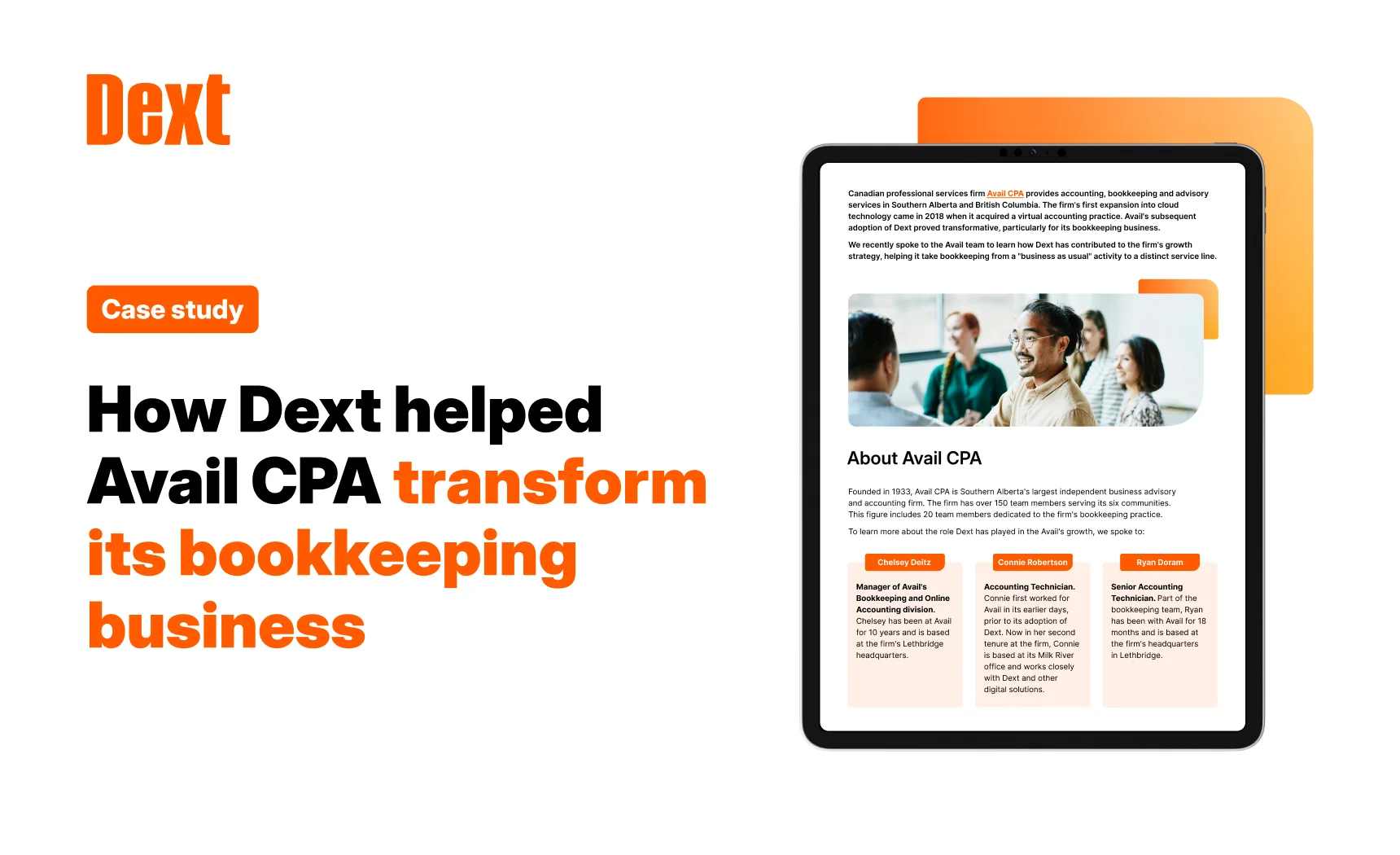

How Dext helped Avail CPA transform its bookkeeping business

Published on: 04.12.2024

The release round-up – Business Owners edition

Published on: 16.10.2024

The release round-up – October 2024

Published on: 03.10.2024

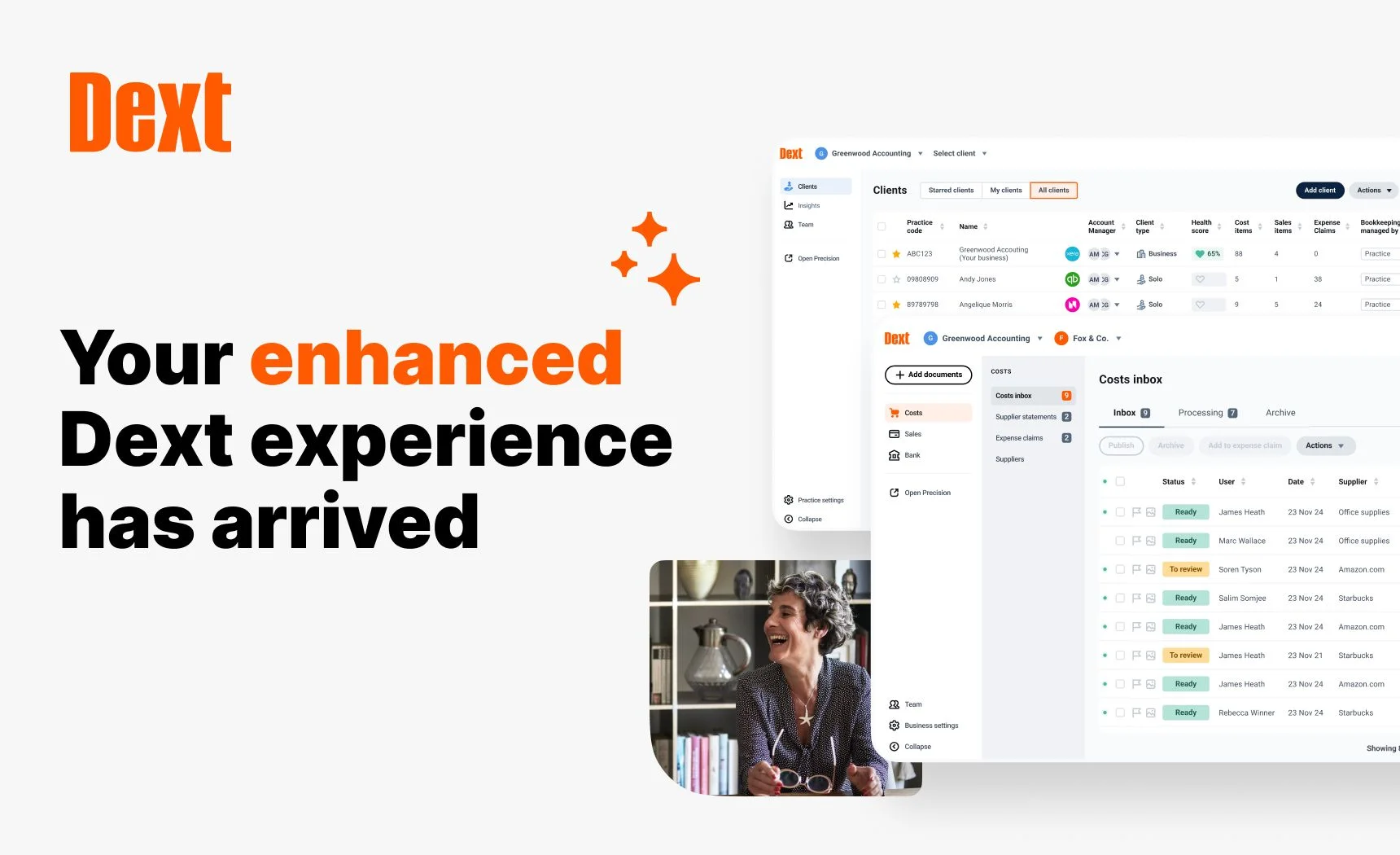

Dext goes live with enhanced user experience

Published on: 18.09.2024

Dext crowned Small Business App of the Year at the 2024 Xero US Awards

Published on: 09.09.2024

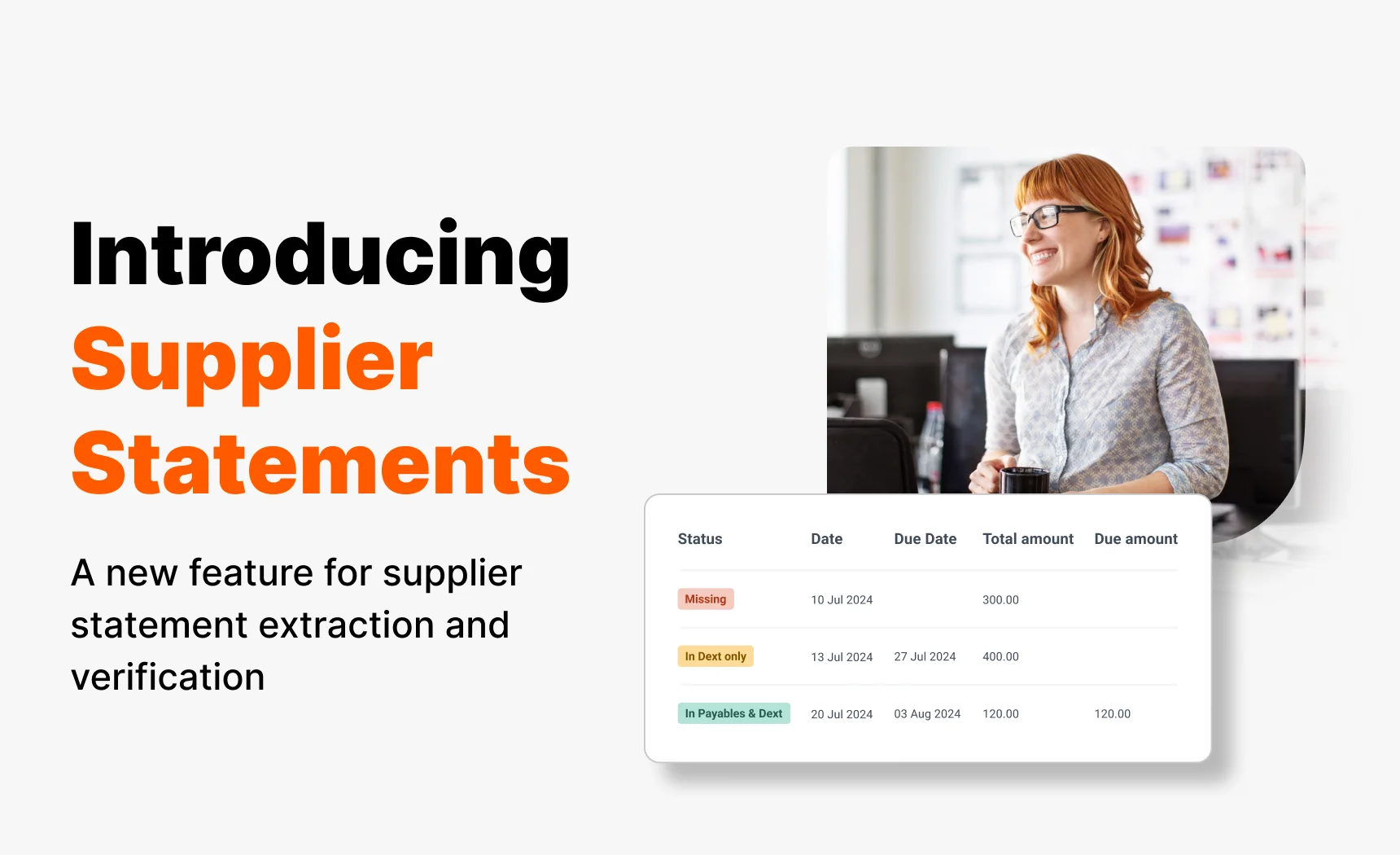

Supplier Statements – Dext’s new feature for supplier statement extraction and verification

Published on: 09.09.2024

How to Streamline Your Company’s Employee Expenses

Published on: 09.09.2024

Understanding Expense Reimbursement For Your Business

Published on: 09.09.2024

All You Need to Know About Sundry Expenses

Published on: 09.09.2024

Bookkeeper: Enhance Your Accuracy and Productivity with Dext

Published on: 09.08.2024

The Release Round-Up

Published on: 09.08.2024

5 Ways Automation Transforms Compliance in Bookkeeping

Published on: 09.08.2024

1

2

3

4

…

20

21

22

Next